Table of contents:

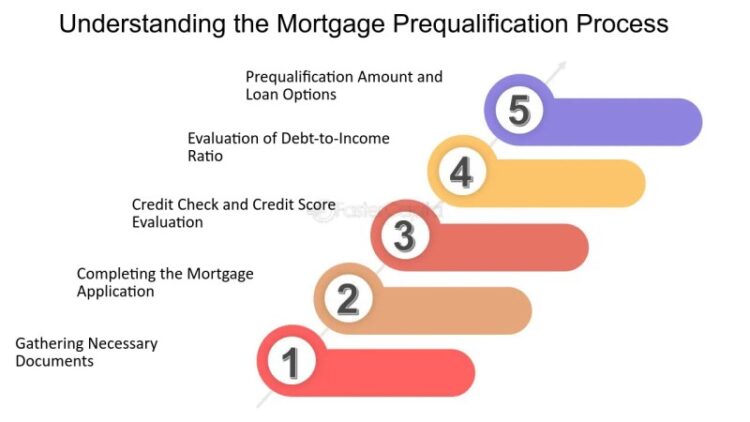

Where To Get Prequalified For A Mortgage – Want to know how the home loan pre-qualification process works? We will prepare 4 steps to inform you of the process. We’ll learn about pre-qualification versus pre-approval, the mortgage approval process and what it means to be pre-qualified.

You need to have a pre-qualification letter and a pre-qualification letter basically means you have a strong financial background and since you have a strong financial background you can prove that you have the funds to buy this house. It pays to make a strong offer and you want to get that house, don’t you?

Where To Get Prequalified For A Mortgage

A pre-qualification is when the lender takes your basic financial information and runs your credit score. That’s it.

Complete Guide To Getting Your Home Loan Approved This Month

So there are actually two types of pre-approvals you can get. The first pre-approval is for the loan officer to approve. And this is where they take your application and ask for additional documents like w-2s, tax returns, and whatever else they need to back up that information in your initial application.

Recommended Reading: The Free First Time Buyer’s Guide Tips for Getting Good Credit The Pre-Qualification Process Making an Offer on a Home Tips What is an earnest money deposit? What is due diligence in real estate? Reasonable request after home inspection. What happens in the week before closing day.

Remember that there are two different types of pre-approval. Therefore, it is a full pre-approval of the pass. Signing means additional steps have been taken to verify the information. With insurance, they actually do more reporting. No one can make this report but themselves. This report is being made so that we can see additional information that needs to be uploaded before closing, as this issue could prevent us from closing.

In closing, whether you’re buying a home, selling a home, thinking about moving to the Orlando area, or just exploring, be sure to get the latest market updates, selling tips, moving hacks, and more on Krish YouTube by following her on Pinterest. , Facebook and Instagram.

Should I Get Pre Qualified Or Pre Approved For A Mortgage?

It gives the smile of living in the city. Portrait of a confident young man out of town When you’re looking for a home, getting pre-approved for a mortgage can be an important step. Consulting with a lender and receiving a pre-approval letter allows you to discuss your loan options and budget with the lender; This step can be used to figure out your overall house hunting budget and what monthly payment you can afford.

As a borrower, it’s important to know what mortgage pre-approval does (and doesn’t) and how to improve your chances.

Think of mortgage pre-approval as a physical examination of your finances. Lenders will probably dig into every corner of your financial life as a way to make sure you pay your mortgage.

You may have heard the term “pre-qualification” used interchangeably with pre-qualification, but they are not the same. With prequalification, you provide the mortgage lender with an overview of your finances, income and debt. The mortgage lender gives you an estimate of the loan amount.

When And Why Should I Get Pre Approved For A Mortgage?

In this way, the mortgage prequalification can be useful in estimating how much you can spend on the home. However, lenders do not pull your credit report or verify your financial information. Accordingly, the pre-qualification is a helpful starting point for determining what you can afford, but it carries no weight when you make an offer.

On the other hand, pre-approval involves filling out a mortgage application and providing your Social Security number for the lender to run a credit check. When you apply for a mortgage there is a tough credit check. For this process, a lender pulls your credit report and credit score to assess your creditworthiness before deciding to lend you money. These checks are recorded on your credit report and can affect your credit score.

Instead, a soft credit check occurs when you pull your credit, or when the credit card company or lender pre-authorizes an offer without you asking. A credit check does not affect your credit score.

You will also list all your bank account details, assets, debts, income, work history, past addresses and other critical details for the lender. This is because, above all else, lenders want to make sure you can repay your loan. Lenders also use the information you provide to calculate your DTI ratio and LTV ratio, which are important factors in determining the ideal interest rate and loan type.

Redondo Mortgage Center

All of this makes pre-approval more expensive than pre-qualification. This means that the lender has checked your credit and checked your documentation to approve the exact loan amount. Final loan approval occurs when the appraisal is done and the loan is applied to the property.

The mortgage pre-approval letter is valid for 60 to 90 days. Lenders put an expiration date on these letters because your finances and credit profile can change. When your pre-approval ends, you’ll need to fill out a new mortgage application and submit updated documentation to get another one.

If you’re thinking about buying a home and you think you’re having trouble getting a mortgage, the pre-approval process can help you identify credit issues and maybe give you time to fix them.

Getting pre-approved six months to a year before serious house hunting puts you in a strong position to improve your overall credit profile. Plus, you’ll have more time to save money for your down payment and closing costs.

How To Get Pre Qualified For A Home Loan

When you’re ready to make an offer, sellers often want to see a mortgage pre-approval and, in some cases, proof of funds to show you’re a serious buyer. In many hot housing markets, sellers have an advantage due to high buyer demand and a limited number of homes for sale; An offer may be considered without a pre-acceptance letter.

Applying for a mortgage can be exciting, nerve-racking and confusing. Some online lenders can get you approved within hours, while others take days. The timeline depends on the lender and the complexity of your finances.

To get started, fill out a mortgage application. Enter your identifying information, including your National Insurance number, so that the credit provider can remove your credit. Although a mortgage credit check is counted as a hard inquiry on your credit report, and can affect your credit score, if you shop around some lenders for a short period of time (typically 45 days for the new FICO model), a combined credit check. considers it as a single query.

This is an example of a uniform mortgage application. If you are borrowing with a spouse or another borrower whose income must be eligible for the mortgage, both applicants must submit financial and employment information. There are eight main parts to mortgage applications.

Mortgage Prequalification Guide

The specific loan products you are applying for; loan amount; conditions, such as the loan repayment period (restriction); and interest rates.

Address; legal description of the property; Year of Production; It is a loan for purchase, refinancing or new construction; and the type of housing in question: primary, secondary or investment.

Your identifying information, including your full name, date of birth, social security number, years of schooling, marital status, number of dependents, and address history.

Name and contact details of current and previous employers (you have been in your current position for less than two years), date of employment, job title and monthly income.

Prequalification Interview: What To Expect When Applying For A Mortgage

List your basic monthly income, as well as overtime, bonuses, commissions, net rental income (if applicable), dividends or interest, and other monthly income, such as child support or alimony.

You’ll also need an accounting of your monthly housing expenses, including rent or mortgage payments, homeowner’s and mortgage insurance, property taxes, and homeowner association dues.

List all bank and credit union checking and savings accounts with balance amounts, as well as life insurance, stocks, bonds, retirement savings and mutual fund accounts and matching values. You’ll need bank statements and investment account statements to prove you have the funds for the down payment and closing costs, in addition to cash reserves.

You should also list all liabilities, including repayment accounts, alimony, child support, car loans, student loans, and other debts.

How To Get Prequalified For A Mortgage: 13 Steps (with Pictures)

Review key transaction details, including purchase price, loan amount, repair/improvement value, estimated closing costs, buyer’s allowance and mortgage insurance (if applicable). (The donor will fill in most of the information.)

Inventory of past judgments, liens, bankruptcy or foreclosures, inventory of pending lawsuits or delinquent debts. You will also be asked to indicate whether you are a US citizen or permanent resident and whether you intend to use the home as your primary residence.

Most home sellers will be willing to negotiate with people who have proof that they can get financing.

Lenders are required by law to provide you with a three-page document called a loan estimate within three business days of receiving your mortgage application. this

Mortgage Pre Approval Vs. Prequalification: What’s The Difference?

Where to get prequalified for a mortgage, get prequalified for mortgage, how to get prequalified for mortgage loan, how long to get prequalified for mortgage, get prequalified for mortgage loan, when to get prequalified for a mortgage, where can i go to get prequalified for a mortgage, get prequalified for mortgage online, get prequalified for a mortgage, how to get prequalified for a mortgage, how to get prequalified for mortgage, steps to get prequalified for a mortgage