Table of contents:

Is It Better To Refinance Or Get Home Equity Loan – With mortgage rates set to double in 2022, homeowners who have run out of time on their mortgage may want to refinance or refinance their existing mortgage.

Is it really a clear decision to opt to refinance or refinance when your current mortgage is about to come out of its lock-in period? Are interest rates the only factor to consider?

Is It Better To Refinance Or Get Home Equity Loan

What are the main factors you should check to make a good decision and what options are available?

How To Tell If It’s Time To Refinance

Usually, the term of the mortgage is proportional to the monthly payments to be paid. Simply put, you have to pay off your mortgage in full in X years:

Some homeowners may choose to extend the term of their loan to better manage their monthly cash flow.

The amount you can borrow (loan value limit) also depends on your (the borrower’s) age. An upper limit is set for the loan amount if the loan period and your age is more than 65 years. For joint loans, the average age is used. For Andrew and Ling, this would look like this:

Most homeowners looking to refinance or refinance their mortgages want to reduce their monthly mortgage payments. However, there are some differences between the 2.

Reasons People Choose To Refinance Their Home Loans

Refinancing means switching to a new mortgage package within the same bank, while refinancing means closing your current mortgage account and taking out a new mortgage from another bank.

For example, when you refinance, you switch to another bank, so there will be at least $3,000 in legal/appraisal fees. When you redo, you’ll get a better rate from your current bank; but they may have to pay a conversion/administration fee which can be around $800.

An early repayment fee may also accrue if you withdraw from your mortgage during the lock-in period. Here’s a rundown of typical costs to help you decide whether to refinance or refinance.

Those who choose to refinance with / POSB will receive a cash discount on loans of at least $250,000 (prefabricated HDB flats) and $500,000 (prefabricated private properties). The minimum loan amount for all mortgage packages is $100,000.

Va Cash Out Refinance Rates And Guidelines For 2023

Homeowners should compare the savings on both options: Refinancing can offer cash discounts that can be used to offset legal and appraisal costs. Alternatively, your current bank may offer payment options. of which give you more savings.

Another consideration is that when a mortgage buyer chooses to refinance instead of refinance, they must:

If you plan to use the extra money (once you have set aside enough emergency funds and insurance), the money in your CPF Ordinary Account (OA) can be kept for retirement planning. After all, your CPF savings earn at least 2.5% annual interest, which shouldn’t be wasted.

Andy and Ling took out a $500,000 mortgage from Bank A for 25 years at an annual interest rate of 4.25%. (fixed) and a lock-in period of 3 years. Now that they are about to come out of lockdown, they are thinking about whether to refinance with Bank A or refinance with Bank B.

The Pros And Cons Of Refinancing A Home

Even if banks A and B offer the same rates, you can save more by pricing the fees. Of course, there are other considerations such as subsidies, processing times, cooperation with other banking products, possible fines and interest rates after the lock-in period that can change the course of refinancing.

Check your detailed mortgage payment with POSB’s payment schedule calculator to see if it makes sense to refinance or refinance

Leaving your confinement period soon? Find out how much you can save by refinancing or refinancing with /POSB.

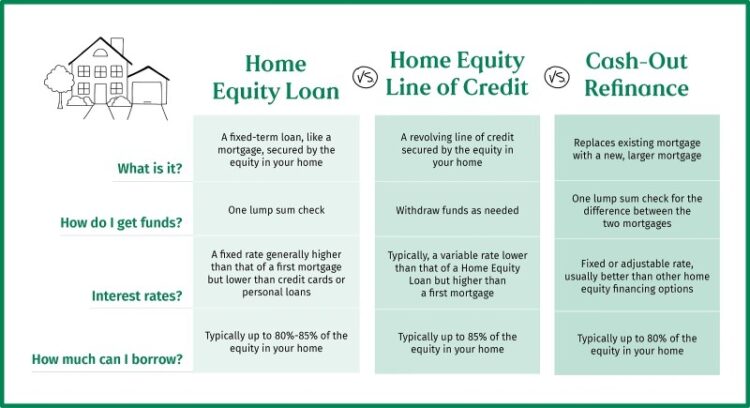

Alternatively, check out other stylish design tools for home ownership. You can even save your detailed real estate budgets and cash flow schedule reports! When refinancing a mortgage, you basically have two options. If you refinance your current loan to get a lower interest rate or change the terms, it is called rate-and-term refinancing. If you want to get some equity out of your home (perhaps to make renovations, pay off debt, or help pay for college), you can apply for a payday loan.

What Is Refinancing?

Think of refinancing as replacing one existing mortgage with another or consolidating a pair of mortgages into a single loan. Out of the old (mortgage) and into the new. After refinancing, old loans are paid off and replaced with new ones.

There are many reasons to consider refinancing. Saving money is obvious. In August 2008, the average interest rate on 30-year fixed-rate mortgages was 6.48%. After the financial crisis, interest rates on similar mortgages fell steadily. In December 2012, the 30-year fixed mortgage rate was cut nearly in half from four years ago, to 3.35 percent.

In 2017, the average annual interest rate increased to 3.99 percent. According to Freddie Mac, it peaked in 2018 at 4.54%, then fell to 3.94% in 2019, and then fell again to 3.11% annually in 2020.

For most people, avoiding the additional cost of a payday loan and getting a loan with interest and term is the best financial move. However, if you have a specific reason for taking money out of your home, a payday loan can be valuable. However, remember that the extra money you pay in interest over the life of the loan could be a bad idea.

How To Get Ready To Refinance

According to Mike Fratanton, vice president and chief economist of the Mortgage Bankers Association (MBA), the reason was “the growing economic impact due to the spread of the corona virus, as well as high volatility in the financial markets.” “

Fratantoni said that “with the national government’s new rate drop this week, we expect refinancing activity to increase further until fears dissipate and rates stabilize.” “These low interest rates are an important factor for homeowners with older, high-interest mortgages, those with home equity appreciation, and those with much better credit scores than when they financed their home. They currently have a house to apply for refinancing now. By December 2020, they had fallen further to 2.68 percent.

When interest rates rise, refinancing can allow you to convert an adjustable-rate mortgage to a fixed-rate mortgage and lock in low-rate payments before interest rates rise even further. However, predicting the future path of interest rates is a major challenge, even for the most experienced economists.

:max_bytes(150000):strip_icc()/dotdash-cash-out-vs-mortgage-refinancing-loans-final-53422e64e4034a31983633db51b0501f.jpg?strip=all "Is It Better To Refinance Or Get Home Equity Loan")

Discrimination in home loans is illegal. If you believe you have been discriminated against because of your race, religion, gender, marital status, use of public assistance, national origin, disability, or age, you can do something. One of those steps is to file a report with the Consumer Financial Protection Bureau (CFPB) or the U.S. Department of Housing and Urban Development (HUD).

Cash Out Vs. Rate And Term Mortgage Refinancing Loans

The simplest and simplest option is financing with interest and terms. In this case, no real money changes hands except for the costs associated with the loan. The mortgage amount remains the same; exchanges the current terms of your mortgage for newer (supposedly better) terms.

On the other hand, in a refinancing loan that was contracted, the new mortgage is greater than the previous one. Along with the new loan terms, you’re also cash positive—effectively taking the equity in your home in cash.

You’ll receive interest and long-term refinancing with a higher loan-to-value ratio (the loan amount divided by the appraised value of the property). In other words, it’s easier to get a loan even if you have a worse credit risk, because you’re borrowing a large portion of the value of the apartment.

Think carefully before taking out a payday loan for investment, it makes no sense to put your funds in a certificate of deposit (CD) that earns 1.58% or even 2.5% when your mortgage rate is 3.9%.

How To Refinance Your House

Retirement loans have stricter conditions. If you want to recover some of the equity you put into your home in cash, it will likely cost you; The amount will depend on the equity you put in the home and your credit score.

For example, if you have a FICO score of 700, a loan-to-value ratio of 76%, and the loan is deemed eligible, the lender may add 0.750 basis points to the original cost of the loan. If the loan amount is $200,000, the lender will add $1,500 to the cost (although every lender is different). Alternatively, you can pay a higher rate: between 0.125 and 0.250 percent more, depending on market conditions.

One more reason to think twice about withdrawals: refinancing withdrawals can negatively affect your FICO score.

However, in certain circumstances, cash loans may not have stricter conditions. A higher credit score and lower loan-to-value ratio can tip the numbers significantly in your favor. If your credit score is, for example, 750 and the loan-to-value ratio is less than 60%, you will not be charged additional costs for the loan taken out. This is because the lender believes you are more likely to default on the loan than if they do a rate and term review.

How Long Does It Take To Refinance A House In 2022?

Your loan may be a cash-out loan, even if you don’t receive cash.

Is it better to get a home equity loan or refinance, what is better cash out refinance or home equity loan, is it better to refinance or get an equity loan, refinance or home equity loan, refinance or equity loan, what's better refinance or home equity loan, is it possible to refinance a home equity loan, which is better refinance or home equity loan, better to refinance or home equity loan, what is better refinance or home equity loan, is it better to refinance your home or get a home equity loan, is it better to refinance or home equity loan