Table of contents:

Government Backed Loans For First Time Buyers – In the middle of securing your first home? Find out the difference between an HDB loan and a bank loan so you can make an informed decision!

As you prepare to buy your first home, start by looking at your financing options – should you opt for an HDB loan or a bank loan? Here are the key differences between the two, so you can choose the one that best suits your needs!

Government Backed Loans For First Time Buyers

An HDB loan requires a down payment of at least 10% of the purchase price, which you can pay in full with secondary account (OA) savings, cash or a combination of cash and OA savings. You need to use your OA savings to buy a flat before taking out an HDB mortgage for the remaining amount. However, you can leave up to $20,000 in OA for your future needs. Apart from enjoying interest on your OA, these savings also act as an emergency fund to meet monthly installments when needed!

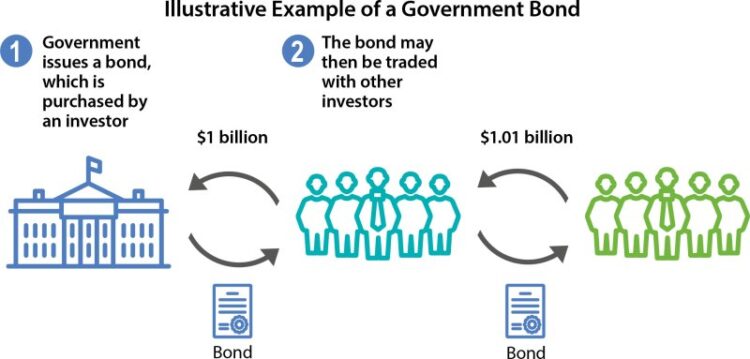

Repurchase Agreement (repo): Definition, Examples, And Risks

If you opt for a bank loan, you will have to pay 20% of the purchase price at the time of signing the lease. 5% is paid in cash, the remaining 15% can be paid in cash or savings. Since a financial institution can borrow up to 75% of the property’s value or purchase price (whichever is lower), you’ll also need to pay the remaining 5% of the purchase price in cash or when you pick up the keys. In your apartment. You also have the option to set the amount you want and pay your mortgage in cash instead.

Bank loan rates are subject to change depending on market conditions, while the HDB loan rate is 0.1% higher than the current OA rate, i.e. 2.6% p.a. If you want to pay less so you have more savings for retirement, a bank loan usually has a lower interest rate than an HDB loan. However, be sure to look into payment options to get the best interest rate!

There is no lock-in period for HDB loans, so there is no penalty if you want to pay off your loan early. This also means that you have the option to renew your loan at the bank at any time if you want to click on one of the lower rates. However, when you renew your HDB loan at the bank, you cannot go back to the HDB loan.

Instead, most banks have a lock-in period, usually two or three years. If you want to repay your loan early or renew your loan to another bank within the lock-in period, you will be charged a penalty, which is usually 1.5% of the loan amount. Similarly, you cannot finance your home with an HDB loan when you have decided to borrow from a bank for your home loan.

Can You Add Renovation Costs To Your Mortgage?

The type of loan you choose, as well as other factors such as the type of apartment and remaining rent, will determine how much savings you can use to buy an apartment.

Find out how much savings you can use to buy an apartment using the Home Use Calculator.

When planning your finances for buying an apartment, it’s important to remember that your savings are also for your pension. You can consider paying off part of your home in cash so that your OA savings can go down to 3.5%, with an attractive interest rate. * To support your retirement plans!

Remember that you need to consider not only your current financial situation, but also your future needs!

The First Time Home Buyer Incentive Is A Failure: Here’s How To Fix It

* With additional benefits. Members under 55 are paid an additional 1% annually on the first $60,000 of their combined balance. Members age 55 and older are paid an additional interest rate of 2% per annum on the first $30,000 and 1% per annum on the next $30,000 of their combined balance. Terms apply. Most people immediately respond to the 20 percent that lenders want new home buyers to put down when buying their first home. With student loan debt, or perhaps just entering the workforce with a low salary, home ownership can be out of reach for many looking for the financial benefits of home ownership.

But I am here to say that for many of my new home clients, I have financed them with a substantial down payment or even no down payment. According to the National Association of Realtors, most first-time homebuyers simply give up and the average stays at 6 percent. Even in California, where home prices are high, that’s a big difference. In some cases you can even leave 0%!

I work with my clients to open up and consider all of their options when purchasing their first home. Many people are surprised to learn that they can actually own a home without a significant down payment. I’ll help you think through your options to decide what makes the most financial sense for you. Staying in touch means I’ll be happy to guide you through the home buying process and find a new home that makes the most financial sense. It is often one’s single largest investment, and most people need a mortgage to buy. The mortgage you get depends on the interest rate, terms, eligibility requirements and ultimately what type of home you can afford. FHA loans and conventional loans are the two most common mortgages.

FHA loans are backed by the Federal Housing Administration (FHA) and offered by FHA-approved lenders. These loans are usually easier to get than conventional loans and have lower repayment requirements. However, you will pay the mortgage insurance premium (MIP) for at least 11 years – which is possible as long as you have a reasonable loan balance.

The Beginner’s Guide To Mortgage Lending

Unlike FHA loans, conventional loans are not guaranteed or guaranteed by a government agency. These loans have stricter credit standards and higher down payment requirements than FHA loans. But Private Mortgage Insurance (PMI) is only required if you put down less than 20%. If this happens, you can ask your lender to cancel PMI when your balance drops to 80% of the home’s original value.

FHA loans and conventional loans allow borrowers to finance the purchase of a home, but they are not the same. Here’s a list of key differences when looking for a mortgage for your next home.

An FHA applicant can get a credit score as low as 500, although 580 is preferred (and most FHA-approved lenders won’t go below that). They have strict requirements for down payment, debt-to-income ratio (DTI) and housing finance ratio. It is also a subprime loan with a higher annual percentage rate (APR) than an FHA loan or conventional loan with a credit score of 580.

FHA loans require a 3.5% down payment if you have a credit score of 580 or higher. However, those with scores between 500 and 579 will have to pay 10 percent. FHA loans can only be used to purchase a primary home.

Best Mortgage Lenders For First Time Buyers Of December 2023

A first-time home buyer can get a customized loan with a down payment of up to 3% of the purchase price. However, to avoid the payment guarantee, you must put 20% down. If you’re not buying your first home and you earn less than 80% of the median income in the area you’re buying, the lower rate is 5%. If you buy a second home, it goes up to 10 percent, and if you buy a multi-family home, it goes up to 15 percent.

The debt-to-income ratio (DTI) compares your income to your debts. Lenders look at this number to see if you can afford to buy a home and get a mortgage payment.

With an FHA loan, the DTI ratio cannot exceed 45% if your credit score is below 580. Most conventional and FHA mortgages require a DTI ratio of 50% or less.

Depending on the terms of your mortgage and the size of your down payment, you may have to pay for mortgage insurance. Unlike other insurance policies, mortgage insurance is unsecured.

First Time Home Buyer Tips

FHA borrowers are required to pay mandatory mortgage insurance premiums (MIPs), regardless of the amount of the down payment. The loan involves a down payment, which can be converted into a loan and paid off with monthly interest for the rest of your life. Borrowers who put down 10% or more pay this premium over 11 years. Anyone paying less than 10% must make these insurance payments for the life of their mortgage.

With conventional loans, you must pay private mortgage insurance (PMI) if you put less than 20 percent down. You can ask your lender to cancel PMI when your mortgage balance is paid off.

Government loans for first time home buyers with bad credit, best mortgage loans for first time buyers, best home loans for first time buyers, government backed mortgages for first time buyers, government loans for first time home buyers, government backed business loans, fha loans for first time home buyers, housing loans for first time buyers, government backed loans for small business, government loans for first time buyers, mortgage loans for first time home buyers, loans for first time home buyers