Table of contents:

Fha Loan And First Time Home Buyer – The federal government has loan programs for homeowners with bad credit scores and no payments. Promoting home ownership – especially for low-income Americans – can be guaranteed through one of its home loan programs. In other words, the government promises the borrower to repay the loan if the borrower defaults.

There are several government agencies that administer mortgage loan programs for Americans, including the United States Department of Housing and Urban Development (HUD) and the Federal Housing Administration (FHA). The terms “HUD loan” and “FHA loan” are often used interchangeably, but there is a difference.

Fha Loan And First Time Home Buyer

HUD oversees the FHA and operates many programs designed to promote home ownership, increase safe and affordable housing, reduce homelessness, and combat housing discrimination. . FHA loans are for home buyers who do not qualify for a conventional loan. HUD does not guarantee a mortgage unless you are an American citizen.

Hud Vs. Fha Loans: What’s The Difference?

HUD’s job is to administer various federal housing programs in the name of promoting affordable and equitable housing. HUD actively supports community development and home ownership through a number of initiatives. It implements the Fair Housing Act and provides housing assistance through the Community Development Block Grant (CDBG) program and the Housing Choice Voucher program, among other programs.

Although HUD guarantees some loans themselves—namely, Section 184 loans, which are available only to African Americans—it is the FHA that single-family homeowners often look to. FHA became part of HUD in 1965.

Section 184 loans are intended for members of Native American and Alaska Native families or designated housing groups. Loans are guaranteed by the Office of Loan Guarantees within HUD’s Office of Native American Programs.

Home buyers must have a minimum down payment of 2.25% for loans over $50,000 and 1.25% for loans under $50,000. Borrowers must pay for home insurance. A fee of 1.5% of the loan amount is payable at closing and the loan can be paid off. In addition, loan-to-value (LTV) ratios of 78% or higher are subject to an annual mortgage insurance fee of 0.25%, paid monthly.

Fha Insured Loan

HUD and FHA do not offer mortgage financing. Instead, you get a loan from an approved lender, such as a bank or other financial institution. Depending on the loan, HUD or FHA guarantees it and pays the borrower if it defaults.

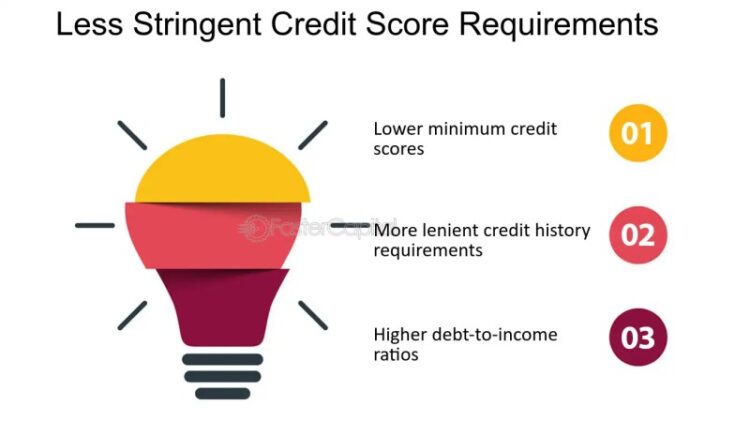

The FHA provides mortgage insurance to qualified borrowers. Its home loan program is designed for borrowers with low down payments and low credit scores. In general, borrowers will find it easier to get an FHA loan than a conventional loan. Lenders do not require a complete credit history. People who have gone through bankruptcy or foreclosure can get an FHA loan, depending on how much time has passed and whether they have good credit.

With an FHA loan, you can borrow up to 96.5% of the home’s value. This means you need to pay 3.5%. You need a credit score of at least 580 to qualify. If your credit score falls between 500-579, you can get an FHA loan as long as you pay 10% down. Subsidized housing must be a primary residence.

All FHA borrowers must pay a mortgage administration fee (MIP) to the FHA—the down payment and the annual fee. Borrowers pay 1.75% of the loan amount – including annual MIPs, which are paid monthly and based on the loan’s value. Borrowers can reduce 10 percent or more to pay in 11 years. Anyone who pays less than 10 percent must make these payments during the life of their loan.

Usda Versus Fha Loan Program Comparison

FHA keeps money from mortgage interest payments (MIPs) in an account that is used to fund the loan program. As a result, it is one of the most independent government agencies, not relying on taxpayers’ money.

HUD’s Section 184 loan program is designed to encourage home ownership among African Americans. Benefits include minimum wage requirements.

Qualified loans are more flexible than conventional loans. For example, interest rates are determined by comparing market rates with the borrower’s credit score.

There are restrictions on small lenders who offer Section 184 loans and the loans are offered in eligible locations selected by participating families. In addition, borrowers must pay for mortgage insurance, which increases the cost of the loan.

There’s Some Hope For First Time Home Buyers

If you have below-average credit and are short on cash for down payments, an FHA insured loan can help you become a homeowner. FHA loans can be chosen for manufactured homes.

Another advantage of FHA loans is that they are secured, which means that the seller of your property can bring it to you, but conventional loans cannot. The buyer must meet the terms of the FHA. Once approved, they take all responsibility for the sale of the goods after the sale of the goods, relieving the buyer of all liabilities.

Although it’s easier to get approved than a regular loan, MIPs increase the overall cost of the loan. That’s why some FHA loan recipients prefer to refinance their property with a conventional bank loan when their credit history improves.

:max_bytes(150000):strip_icc()/FHAnew-V1-b23f55ab8e61496d87eabfccaa25c254.png?strip=all "Fha Loan And First Time Home Buyer")

Mortgage discrimination is illegal. If you feel you are being discriminated against because of your race, religion, gender, marital status, use of public assistance, race, disability, or age, there are steps you can take. One such step is filing a report with the Consumer Financial Protection Bureau (CFPB) or HUD.

How Much To Put Down On A House

FHA-backed loans are part of HUD’s mandate to promote homeownership. There may be different types of government-backed loans. There are two other types of loan programs sponsored by government agencies—the United States. Department of Veterans Affairs (VA) loans and US Department of Agriculture (USDA) loans – so it may be worth researching all options.

When considering any type of home loan, every borrower should consider all the costs. A mortgage will come with interest to be paid over time, but that is not the only cost. All types of mortgage loans have different types of fees that may be required or included in the loan payment.

Also, remember that mortgage payments and mortgage insurance can provide a tax break from any type of loan, but most of them are tax deductible.

The US Department of Housing and Urban Development (HUD) Section 184 loans are available to African Americans to purchase a home as a primary residence. The loans are sponsored by HUD and are intended to encourage home ownership among African Americans.

Keyword:lower Payment Requirements

A Section 184 loan can be used to purchase or construct a home. It can be used to renovate a home or renovate an existing home.

Federal Housing Administration (FHA) loans are guaranteed by the government and are designed for homeowners with below average credit and no money to make a large down payment. FHA loans are offered by FHA approved lenders.

Authors must use primary sources to support their work. These include white papers, official memos, case reports, and interviews with industry experts. We also publish original research from other reputable publishers where appropriate. You can learn more about the practices we follow to publish accurate and unbiased content in our editorial policy. A home is the largest investment a person makes, and many people want a mortgage to finance the purchase. The type of loan you get depends on your salary, terms, eligibility requirements, and the type of home you can afford. The two most common types of mortgages are FHA mortgages and conventional mortgages.

FHA loans are backed by the Federal Housing Administration (FHA) and offered by FHA-approved lenders. These loans are more flexible than conventional loans and have lower down payment requirements. However, you will be paying mortgage insurance premiums (MIPs) for at least 11 years – even when you have the money for the loan.

Do Fha Loans Require Escrow Accounts?

Unlike FHA loans, conventional loans are not regulated or guaranteed by a federal agency. These loans have stricter credit standards and higher interest rates than FHA loans. But private mortgage insurance (PMI) is only required if you put down less than 20 percent. If this happens, you can ask the lender to waive PMI when your payment drops to 80 percentage of the original home value.

Both FHA loans and conventional loans allow borrowers to finance the purchase of a home, but they are not the same. There are several important differences to consider when looking for a loan for your next property.

An FHA applicant can have a credit score as low as 500, although 580 is preferred (and most FHA-approved lenders won’t go lower than that). They have a significant impact on your down payment, debt-to-income ratio (DTI) and home equity ratio. A subprime loan, which means the annual percentage rate (APR) is higher than an FHA loan with a credit score of 580 or a conventional loan.

FHA loans require 3.5%

Fha Home Loan

Fha loan florida first time home buyer, fha loan first time home buyer definition, first time home buyer fha loan qualifications, fha first time home buyer loan application, fha loan first time home buyer california, fha first time home buyer loan calculator, fha loan first time home buyer grants, fha 203k loan first time home buyer, fha loan first time home buyer requirements, fha loan texas first time home buyer, fha loan first time home buyer, first time buyer fha loan